.png)

For a century, value in the electricity system was created upstream: it was about producing, transmitting, and distributing kWh. The players who controlled these physical assets captured most of the rent. The energy transition is not just about substituting production sources. It shifts the center of gravity of value downstream, towards software and relational layers that historical players don't always master, in a context where dependence on fossil fuel imports remains the primary vulnerability of the European electricity system.

This underlying trend is confirmed : in France, alternative suppliers have gained over half a million new residential customers in one year, accelerating their progress and consequently reducing the scope of regulated tariffs, the historical foundation of the system.

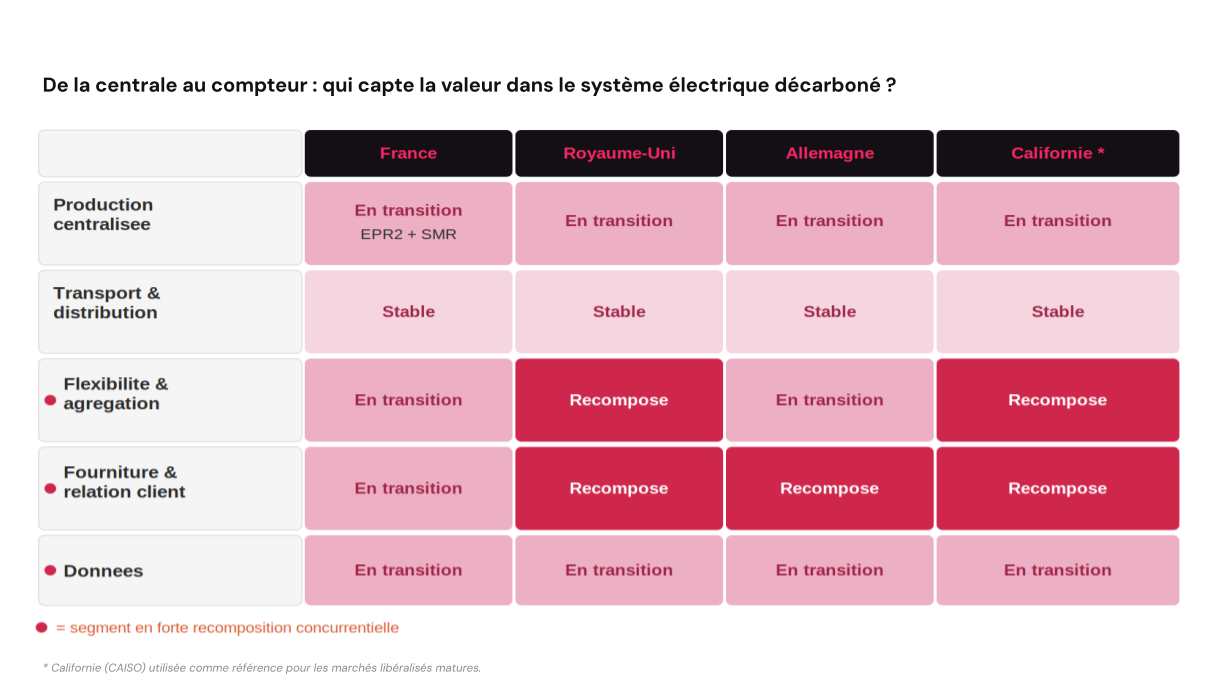

The chain remains clear in its main stages: generation, transmission, distribution, supply, consumption. However, competitive intensity is no longer uniform along this chain. Some segments remain stable, while others are rapidly reconfiguring.

Centralized generation, particularly nuclear, maintains a strong position in France, supported by irreplaceable short-term assets, even if the relaunch of EPR2 reactors and the acceleration of SMRs signal a profound technological transformation in the medium term. Regulated transmission and distribution networks are evolving under investment pressure: 30 GW of access rights already allocated for industrial projects, data centers, and hydrogen production, signaling future demand not yet fully reflected in tariffs.

But the transformations are even stronger in the other three segments: flexibility, customer relations and services, and data.

The frequency of negative or zero prices in the European wholesale market has been multiplied by 18 between 2022 and 2024. This is not a cyclical anomaly. It is the structural signal of a system that is producing more and more less dispatchable electricity: in 2025, wind and solar produced more electricity than all fossil sources combined in 14 of the 27 EU countries. Daily flexibility needs are expected to more than double by 2030. Value is no longer created solely by producing: it is created by managing when and how we consume. This is precisely the domain of aggregators and VPP operators (three recent analyses from Zenon), new entrants who integrate into the chain without necessarily owning a single electrical cable.

The transformation of the end customer's role — from passive consumer to dispatchable asset — is accelerating: the number of smart electricity tariffs and services available to European consumers has almost tripled in three years. However, this potential remains largely untapped : inflexible contracts remain dominant in most member states. The demand-side response accounted for 10% of total European flexibility in 2024 and could reach 21% by 2030. Alternative suppliers who master customer relationships and optimization algorithms are capturing an increasing share of value without having to finance physical assets. This dynamic is fully evident in France, where the shift towards players without historical physical assets is accelerating .

This shift towards market-based offers makes the issue of metering data sharing all the more crucial. Enedis holds the data from 37 million Linky meters. Access to this data is regulated, partially open, and fiercely negotiated. The CRE deliberation of July 2025 on the valuation of demand response marks real progress, but activated volumes remain low. This delay is not unique to France. Who will control granular real-time consumption data, and under what conditions will they share it with third-party aggregators? Access to granular Linky data could become a decisive competitive advantage for new entrants looking to offer flexibility solutions truly tailored to consumption profiles.

The figure describes the intensity of competitive recomposition in each segment, regardless of the technological and operational transformations underway across the entire chain.

Sources: ACER-CEER MMR 2024 and Rewarding Flexibility 2025 · Ember EER 2026 · McKinsey 2025 · RTE BP 2025 · CRE 2025 · FERC Order 2222 California* CASIO/FERC Order 2222

Incumbent players are not doomed. They possess the infrastructure, licenses, and regulatory trust. However, marginal value is now created at the intersection of physical and digital.

A political risk worth highlighting: if value capture focuses on the connected assets of affluent households, flexibility will reproduce inequalities in energy access . Regulatory signals in the United States or in France) indicate that regulators have chosen to open this market to competition. As the European dependence on imported gas makes every fossil fuel price peak more costly, this opening also becomes an issue of energy security.