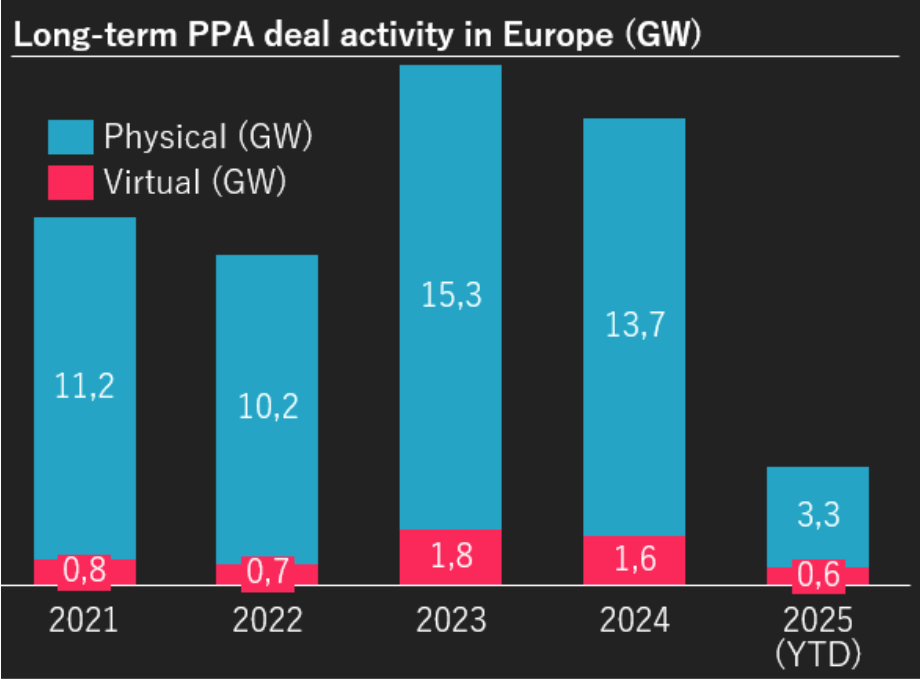

The European Direct Power Purchase Agreements (CPPA) market is experiencing impressive growth: nearly 19 GW signed in 2024, which is a record, with more than 80% concluded by companies. These contracts offer a double promise: to stabilize the price of electricity in a context of high volatility, and to contribute directly to the financing of new renewable capacities. But behind the enthusiasm, questions remain: are CPPAs really the structuring tool we are waiting for, and what future do they shape for European energy balance?

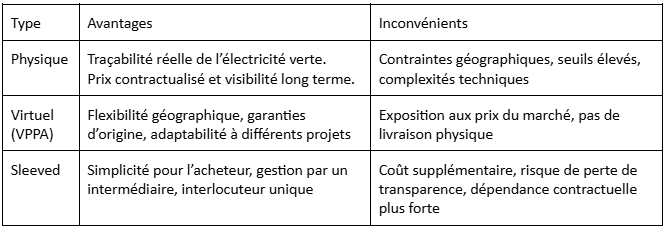

A CPPA, for Corporate Power Purchase Agreement, is a long-term agreement between a renewable electricity producer and an industrial or tertiary consumer. Unlike Utility PPAs, signed with energy suppliers, CPPAs are directly concluded by companies wishing to secure their energy costs and to green their mix. The buyer benefits from a stable price, the producer benefits from guaranteed income, and the energy transition benefits from support for the deployment of new projects. Three models dominate today, each with its own logic.

- The Physical PPA is based on a real delivery of electricity between the producer and the consumer. It offers clear traceability and reinforces the credibility of the climate approach, but assumes that both parties are connected to the same network area. Its management is complex, because the intermittency of production must be compensated, and it remains especially accessible to large manufacturers.

- The Virtual PPA (or VPPA) adopts a financial logic: the company is committed to a reference price and compensates for differences with the market, while receiving original guarantees. It offers great geographic flexibility and adapts to diversified portfolios, but is directly exposed to the vagaries of wholesale markets. This model appeals to multinationals capable of absorbing this risk, minus medium-sized players.

- The PPA Sleeved constitutes an intermediate formula. The contract is signed directly between the producer and the consuming company, but an energy supplier acts as an intermediary to manage delivery, balancing and billing. This intermediation simplifies management for the buyer and makes it possible to maintain traceability and the contractual relationship with the producer, unlike a Utility PPA, where the company does not have a direct relationship with the power plant. However, the sleeved PPA generates additional costs and greater contractual dependence.

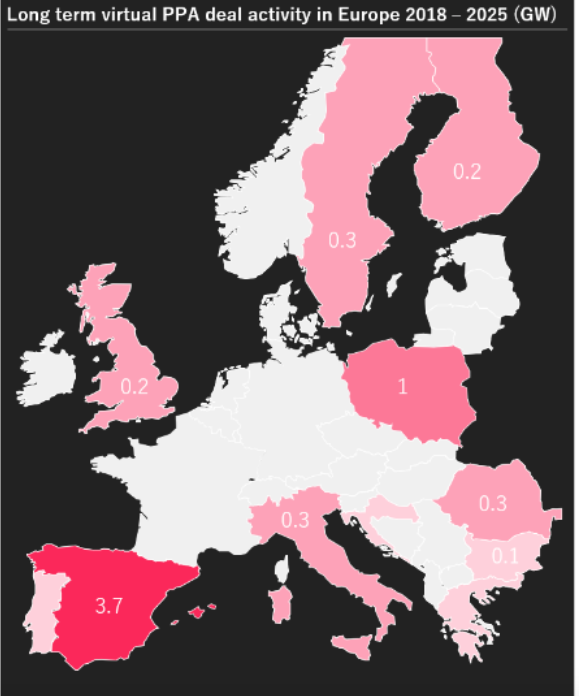

While these three models reflect a growing maturity of the market, their coexistence also fuels fragmentation that can cloud readability for novice players. And recent figures remind us that the trajectory is not linear: in the first half of 2025, CPPAs have down by 26% in volume and 31% in number compared to 2024. Only solar has progressed, with 4.2 GW signed, led by Italy (+184%) and Spain (+51%), while Germany (-88%) and France (-57%) stalled.

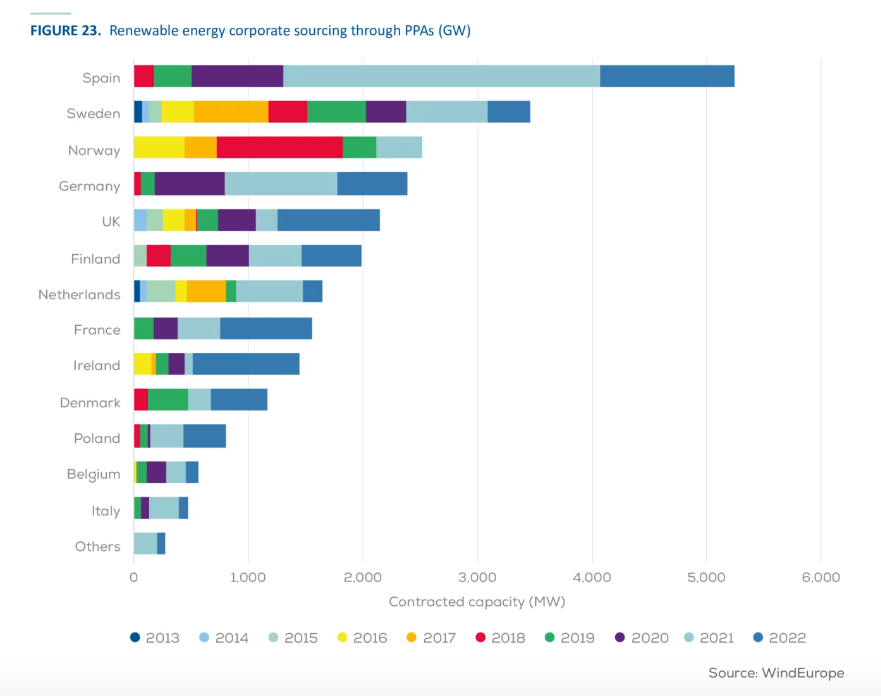

Three challenges then appear. The first concerns accessibility: only large solvent groups benefit from these devices, while SMEs struggle to take the plunge, despite a 500 million euros counter-guarantee mechanismlaunched by the EIB in 2025. The second is linked to persistent volatility: CPPAs partially protect, but do not remove risk. Finally, the relationship with public policies remains unclear: Contracts for Difference (CfD), which also stabilize producers' incomes, could compete with these private initiatives.

The future of CPPAs will therefore depend on their ability to open up and innovate. An emerging path is that of “24/7 contracts”, which no longer guarantee only an annual volume, but an hourly equivalent between consumption and renewable production. To achieve this, they rely on battery storage and, tomorrow, on green hydrogen, capable of compensating for intermittency. This new generation of contracts could transform CPPAs into a real energy standard for low-carbon industries, provided they overcome their current barriers and do not remain reserved for the best equipped multinationals.